And why there is little hope for explosive growth in foreign investment

Every loan agreement between Ukraine and the International Monetary Fund (IMF) is accompanied by a memorandum. It is a document that describes in detail the economic realities of the debtor (which is Ukraine), as well as the obligations that our country has undertaken to the Fund.

In general, the IMF is quite conservative about the prospects of the Ukrainian economy. The main problem is that Ukraine is deeply mired in debt and will need hundreds of billions of dollars to eliminate the consequences of the war. Although the Fund, along with other international partners, is ready to provide financial support, the Ukrainian authorities will have to make enormous efforts to mobilise domestic resources for post-war economic recovery and create fertile ground for investment.

Mind has looked into the main points of the memorandum with the IMF and what the new $15.6bn loan from the Fund obliges Ukraine to do.

Key macroeconomic forecasts from the IMF. Several dozen pages of the memorandum are devoted to the situation in the Ukrainian economy and an assessment of its key indicators. In general, the forecasting horizon covers the period up to 2030. However, since the IMF-Ukraine cooperation programme is designed for four years, we will analyse this period in detail.

1. Economic growth will start accelerating no earlier than 2025. In 2023, according to IMF estimates, Ukraine’s GDP will fall by another 3% at worst (after falling by more than 30% in 2022), and at best it will grow symbolically by 1%. In 2024, GDP growth will be 3.2%, and in 2025-2027 – 6.5%, 5% and 4%, respectively.

Ukraine’s GDP growth forecast (baseline and adverse scenarios)

Source: IMF data

2. Inflation in 2023 (year-on-year) will be 20%, which is not much less than in 2022 (26.6%). Consumer price growth will not reach its target level of around 5% per annum until 2027.

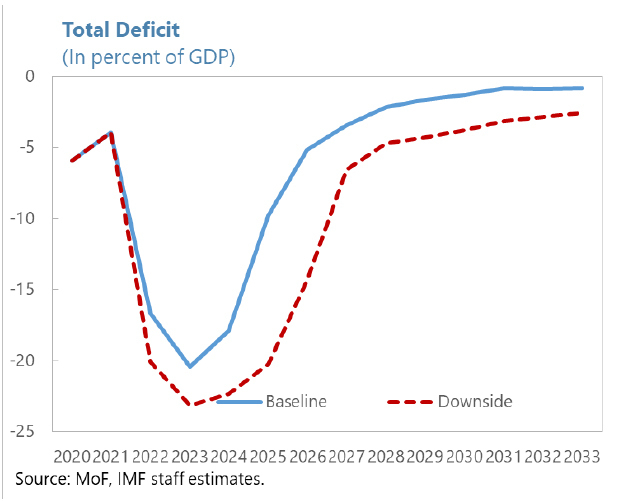

3. The state budget deficit will be significant for quite some time. For comparison, let’s take 2021 as a starting point, when the budget deficit (excluding external grants) was 4% of GDP. In 2023, the deficit to GDP will be 28.2%, in 2024 – 22%, in 2025 – 12%, and only in 2026-2027 will it be reduced to almost pre-war levels of 4.6-6.5% of GDP.

Forecast of the state budget deficit of Ukraine (baseline and adverse scenarios)

Source: IMF data

4. Due to this deficit, Ukraine will continue to be heavily dependent on external financing. In 2023, its volume to GDP will be 19.8%, in 2024 – 17.7%, and in 2026 – 9.5%. At the same time, the IMF forecasts that in 2023, Ukraine’s public debt will exceed 98% (82% in 2022), and in 2024 it will exceed 100% and remain above this limit until 2027 inclusive.

5. Tax revenues will be in the range of 36-39% of GDP in the next few years. The tax part of the state budget revenues will be made up of personal income tax and corporate income tax (10-12% of GDP), as well as consumption taxes, primarily VAT and excise taxes (13-15% of GDP).

Forecast of tax revenues to the Ukrainian state budget (baseline and adverse scenarios)

Source: IMF data

6. Foreign trade will remain deeply in deficit. The negative balance of export and import of goods will grow from $25 billion in 2023 to $35 billion in 2027. The reason is that import will grow at a rate that outpaces export growth. The reason is that it will take a lot of money and time to rebuild the destroyed industries. Therefore, according to IMF estimates, the foreign trade deficit will not be significantly reduced even by 2030.

7. According to the Fund’s calculations, Ukraine should not expect an investment boom either. Foreign direct investment in 2023-2024 will amount to 0.4% of GDP at best, 2.4% in 2025, and close to 5% in 2026-2027.

The IMF’s alternative ‘bad’ scenario indicates that the state of the Ukrainian economy directly depends on how the situation at the frontline develops. Moreover, based on the baseline scenario, on which all the above forecasts are based, the end or at least the decline in hostilities should occur in mid-2024.

At the same time, the fund believes that the risk of further escalation of the military conflict is extremely high, which in turn will lead to a deterioration in the macroeconomic situation. These include new destruction of production facilities, disruption of supply chains, stagnation of foreign trade, another wave of refugee outflows abroad, and a complete freeze on investment (although there is none anyway).

Risk of escalation of the military conflict in Ukraine and its consequences

Source: IMF data

In this case, the second, unfavourable scenario for the Ukrainian economy could be realised. This scenario implies that the GDP decline will continue, reaching 10% in 2023 and 2% in 2024. GDP growth of at least 4% is possible no earlier than 2027. Inflation will accelerate to 32.5% in 2023 (year-on-year) and 20% in 2024.

The state budget deficit will increase to 35.4% of GDP in 2023 (excluding grant support), and will decline slightly to 32.2% in 2024. Ukraine’s external financing needs in 2023-2024 will be at 21-22% of GDP. It is twice as high as in 2022.

The total financing gap under the adverse scenario will reach about $140 billion, which is about $25 billion more than under the baseline forecast for 2023-2027. The IMF does not exclude that extraordinary measures will have to be taken in this case. These may include new types of taxes (a surcharge on the current personal income tax rate, additional excise duties, etc.), as well as administrative intervention by the NBU in the domestic debt market, which will be manifested in the obligation of banks to buy back a certain amount of domestic government bonds to finance the budget deficit.

Thus, the second, unfavourable scenario could set back Ukraine’s economic recovery by at least two to three years. And its dependence on external financing would increase even further, as the level of public debt could reach 150% of GDP by 2026-2027.

Public debt forecast (adverse scenario)

Source: IMF data

The IMF’s ‘homework’ for Ukraine and its purpose. Ukraine’s commitments under the IMF’s new loan programme are largely focused on ensuring current and medium-term fiscal stability, as well as preparing the ground for post-war economic recovery.

The Ukrainian side, in particular, has committed to take measures to expand investment opportunities, strengthen the energy sector, return to a flexible exchange rate, reduce dependence on external financing, and bring Ukrainian tax legislation closer to EU legislation once active hostilities have abated. The widespread fight against corruption is also mentioned as a ‘beacon’. However, it is a traditional point that appears in every new memorandum.

By the summer, the parliament should vote on draft law No. 8401, which provides for the abolition of the 2% preferential rate for single tax payers (it was introduced in March 2022), the resumption of full-fledged tax audits and the return of fines for businesses for violations related to the use of payment transaction recorders (PTRs). The Cabinet of Ministers and MPs also need to solve the issue of accumulating tax arrears that amounted to 1.5% of GDP at the end of 2022.

At the same time, the Ukrainian authorities assured the IMF that there would be no measures aimed at “reducing and undermining tax revenues” in the coming years. In other words, no lower rates and no exemptions.

Furthermore, plans to eliminate tax avoidance practices through the simplified taxation system (the so-called salaries of individual entrepreneurs), to completely cleanse the tax and customs authorities of systemic corruption, and to strengthen the fight against tax evaders (the Bureau of Economic Security is to be rebooted) are among the priorities for filling the state budget in the post-war period. Tax reform is also planned to “balance the need to ensure the revenue base of the state budget with the interests of business and investors”.

As early as 2023, Ukraine will move to medium-term budget planning and will make a separate forecast of budget revenues and expenditures for 2025-2026 when preparing the draft state budget for 2024. A public debt management strategy should be ready by September 2023.

In short, Ukraine is committed to strengthening the domestic debt market, attracting not only banks (currently one of the main buyers of government bonds) but also non-residents. The goal is to prevent emission and reduce the state budget’s dependence on external aid, replacing it with domestic financing.

At the same time, the Ministry of Finance will prepare and submit the National Revenue Strategy for 2024-2030 to the Cabinet of Ministers for approval. It is a comprehensive document that will contain the main principles and directions of fiscal (tax, budget, debt) policy. The strategic goal is to accumulate all possible resources for post-war recovery.

We will have to do everything on our own. The main conclusion to be drawn after analysing the memorandum with the IMF is that we should not expect rapid economic growth after the war is over. At the same time, Ukraine needs to prepare for a long and difficult recovery. In more detail, the main results are as follows:

- The best-case scenario is a cessation of hostilities (or their suspension) around mid-2024, while the worst-case scenario is a prolonged war that could last for years and destroy the Ukrainian economy.

- Even with annual economic growth of 3-4%, by 2027, Ukraine will reach 75-80% of its GDP in 2021. Thus, we still won’t be able to return to the pre-war state in five years.

- Unfortunately, we should not rely on external investors. International assistance (from the IMF in particular) is intended mainly to balance the state budget. At the same time, the volume of FDI, according to IMF estimates, will be in the range of $5-10 billion per year. It is very little, given that Ukraine’s direct losses due to the war alone, according to the Kyiv School of Economics (KSE), amount to almost $140 billion.

- It all comes down to the fact that the country will have to rebuild itself largely on its own. Of course, the economy cannot be restored on government bonds alone. Consequently, the role of the state apparatus will be strengthened, on the one hand (expanding the powers of supervisory authorities), and fiscal pressure (tax increases) will increase, on the other. Moreover, it is likely that many tax innovations will be presented under the pretext of the need to reform the tax system for Ukraine’s accession to the EU.